Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

If Denver is the heart of the metro, Aurora and Parker are the two arms stretching out toward families who want space, good schools, and a slower rhythm.

Both are growing fast. Both are packed with parks, trails, and family-friendly pockets. But they each have a different flavor — like choosing between two great coffees. Same caffeine. Different vibe.

Let’s break it down.

Living in Aurora

Aurora is huge — one of the most diverse, exciting, and fast-growing cities in Colorado.

It offers:

-

A wide range of home prices

-

Top-rated schools in areas like Cherry Creek

-

Easy access to DIA

-

Tons of new development

-

Great for families wanting affordability + location

-

Beautiful outdoor areas like the Reservoir, parks, and trails

Aurora is perfect for families who want convenience and community without being far from Denver.

Living in Parker

Parker is like the charming storybook suburb where every weekend feels like a small-town festival.

You get:

-

Award-winning Douglas County schools

-

Big yards

-

Newer homes and master-planned communities

-

A cute downtown with boutiques and restaurants

-

A slower, family-focused lifestyle

Parker feels cozy, clean, and organized. Families love it because it’s quiet, safe, and full of community events.

Which one is right for you?

Choose Aurora if you want:

-

Proximity to Denver

-

More price points

-

Diversity in neighborhoods

-

Quick access to the airport

-

Established + new build mix

Choose Parker if you want:

-

Top school districts

-

Suburban calm

-

Newer homes with more space

-

A very family-friendly lifestyle

-

That small-town charm

Both are amazing — it really just depends on your rhythm.

Need help deciding? I’ve helped dozens of families relocate to Aurora and Parker, and I can break down which neighborhoods match your lifestyle.

![Should I Rent or Should I Buy? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/07/14124050/20220715-MEM-1046x2129.png)

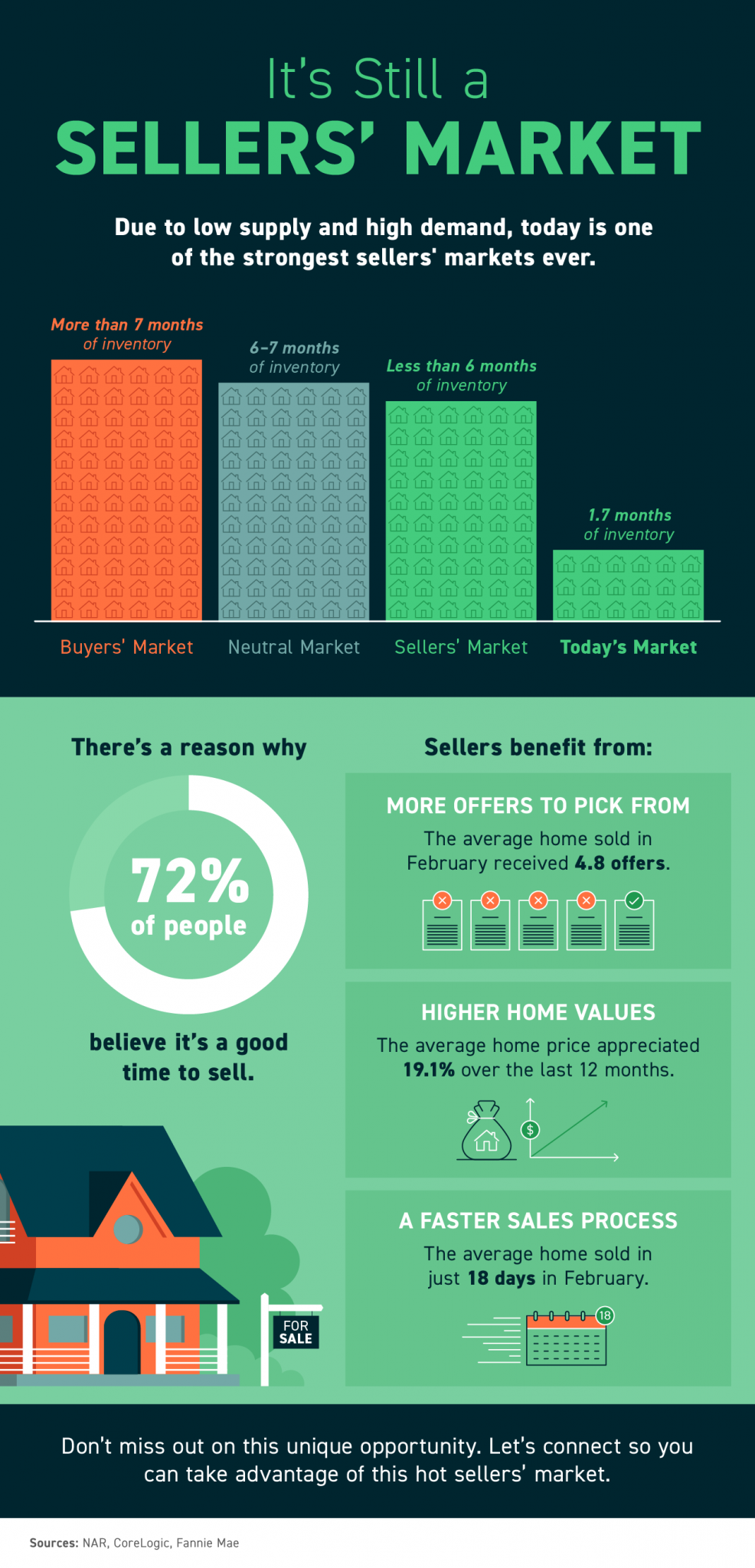

![It’s Still a Sellers’ Market [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/04/31142157/20220401-MEM-1046x2173.png)